Forget the days of trekking to a branch to borrow money – financial services are now offered digitally and, increasingly, seamlessly embedded into our everyday experiences. The global embedded finance market is projected to grow five times, from $54.3 billion in 2022 to an estimated $248.4 billion by 2032. Its potential has led an Accenture and Plaid report to hail embedded finance as one of the top five financial innovations in the last 50 years.

As embedded finance transforms services like payments and lending, banks and payment service providers (PSPs) face both lucrative opportunities and disruptive challenges. Should banks and PSPs try to capitalize on potential revenue growth despite the risks?

Table of Contents

What is Embedded Finance

Embedded finance refers to incorporating financial services into a non-financial customer journey or platform, like providing financing options on an e-commerce site. For example, businesses can embed point-of-sale lending by offering Buy Now, Pay Later, which splits up purchases into installments.

With embed finance, companies increase the number of touchpoints to offer financial products and address consumer expectations for on-demand services. 88% of companies that have implemented an embed finance feature see increased engagement and 85% say that it helps them acquire new customers.

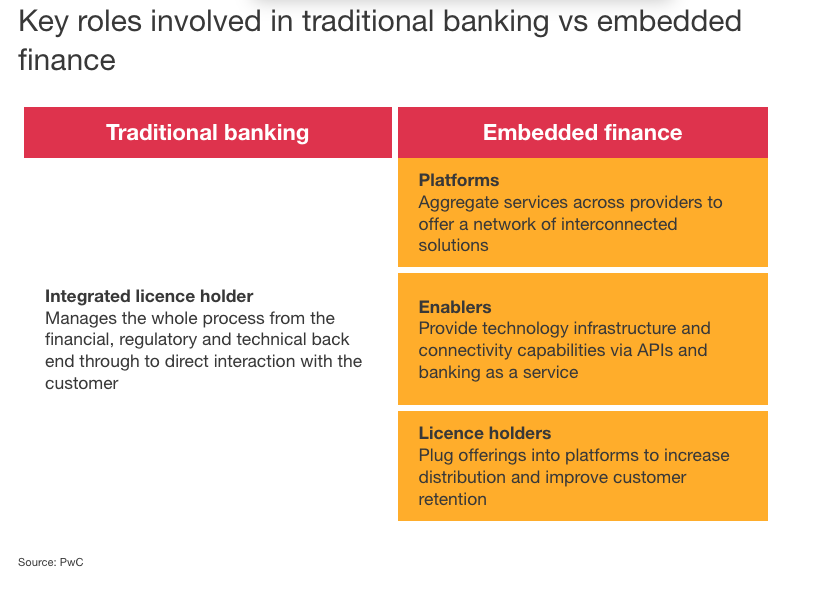

However, embedded finance also reflects a paradigm shift in the traditional banking model, where one license holder manages the entire product offering from a financial and regulatory standpoint all the way to customer engagement. Instead, embedded-finance usually combines license holders with platforms that consolidate interconnected services and enablers that provide the technology infrastructure via APIs.

How Embedded Finance Is Shaking Up the Payments Landscape

Over 70% of banks still view embedded finance as a threat, wary of sharing customer relationships with newer players. As a result, retail banks continue to lag in the ability to offer the personalized omnichannel experiences that customers crave. So far, fintechs have taken the lead in embracing embedded finance, diverting an estimated $8 to $10 billion in annual revenue away from banks, according to McKinsey.

Although embedded finance broadly encompasses products ranging from lending and payments to integrated insurance and investing tools, payments remain the biggest driver of revenue. The total volume of payments facilitated through embedded-finance channels skyrocketed to $2.5 trillion in 2021. Projections call for that figure to surpass $6.5 trillion by 2025 as adoption accelerates.

Between surging payment volumes and innovative products, embedded-finance rapidly disrupts traditional banking and payment processing. Providers that don’t adapt risk losing customers and transactions.

The Embedded Finance Opportunity

The shifting landscape offers players like banks and neobanks, PSPs, and independent software vendors the chance to participate in a growing opportunity set. Potential upside comes from:

- Additional Revenue Potential. Lightyear Capital estimates that embedded offerings could generate over $230 billion in additional revenue globally by 2025 for financial service providers. Venture capital firm Andreessen Horowitz estimates embedded tools can multiply customer revenue by 2-5x.

- Comprehensive Solutions. PSPs have begun offering solutions that go beyond embedded payments that lower friction. More PSPs are also embedding transactions, reconciliations, and data analysis into merchant ERP systems and adding significant value. PSPs that offer these solutions can charge higher prices per transaction and gain market share.

- Increase Distribution and Loyalty. Banks reach new markets and customers through embedded products integrated into partner ecosystems. Increased distribution and highly relevant financial offerings also build loyalty with existing clients.

Navigating the Risks and Challenges

Despite the substantial upside of embedded finance, embracing the evolving market requires foresight, agility, and strategic collaboration.

- Mindset shift. For banks, embedded models require a mental leap away from owning every customer engagement. However, providers like banks, neobanks, and ISVs have the opportunity to focus on their core competencies while expanding capabilities and distribution through embed finance.

- Strategic Partnerships. Banks and PSPs must carefully vet partners to implement embedded products that complement their business models. For example, a traditional third-party BNPL provider like Affirm or Klarna diverts transaction volume away from payment processors. The right BNPL partner expands payment offerings but allows you to process payments on your own rails without siphoning away transaction volume. Ultimately, strategic partnerships can be a win-win for financial institutions that want to reach more customers and PSPs looking to provide comprehensive solutions.

Capitalize on Embedded Finance Opportunities with Strategic Partners

The rise of embedded finance presents a pivotal moment for financial institutions and PSPs. Although risks exist, the potential benefits are too great to ignore— additional revenue, expanded capabilities, lower costs, and increased customer loyalty.

Forging the right partnerships is the key to winning the embedded finance race. Yet 35% of non-financial companies struggle with finding the right partners – making it a key stumbling block to offering embedded finance.

Gratify partners with banks, payment processors, ISVs, ISOs, and merchants directly to offer the convenience of BNPL without redirecting transaction flows and revenues. Explore providing a frictionless customer experience using our white-label embedded finance solution today.

FAQs: Embedded Finance

What is embedded finance?

Embedded finance is the seamless integration of financial services into the platforms of non-financial businesses, allowing these companies to offer banking, payment, lending, and insurance products directly to their customers within their ecosystem.

What is an example of embedded finance?

An example of embedded finance could be an e-commerce platform offering buy now, pay later options at checkout. This allows customers to spread the cost of their purchases over time without leaving the merchant’s site.

How does embedded finance work?

Embedded finance works by non-financial companies partnering with banks and fintech firms to integrate financial services into their existing platforms. This integration enables customers to access and use these services conveniently during their interaction with the non-financial company’s product or service.